How DSCR Loans Help Investors Scale Faster (Even with High Debt or Low Income)

Debt Service Coverage Ratio (DSCR) loans are a specialized type of financing designed primarily for real estate investors looking to grow their portfolios, even in situations characterized by high debt loads or low income streams. The term DSCR refers to a financial ratio that measures the ability of an entity to cover its debt obligations from the generated income. In essence, this ratio serves as an indicator of the cash flow available to pay current debt obligations, providing lenders with a clear perspective on a borrower's financial health.

Howard Hubbard

1/17/20265 min read

Understanding DSCR Loans

Debt Service Coverage Ratio (DSCR) loans are a specialized type of financing designed primarily for real estate investors looking to grow their portfolios, even in situations characterized by high debt loads or low income streams. The term DSCR refers to a financial ratio that measures the ability of an entity to cover its debt obligations from the generated income. In essence, this ratio serves as an indicator of the cash flow available to pay current debt obligations, providing lenders with a clear perspective on a borrower's financial health.

To calculate the DSCR, one must divide the net operating income (NOI) by the total debt service. For instance, if a property generates $100,000 in NOI but has a total debt service requirement of $80,000, the DSCR would be 1.25. This indicates that the property generates enough income to cover its debt obligations and still has a buffer. Typically, lenders expect a DSCR of at least 1.2, representing a margin of safety for loan repayments. However, specific threshold requirements may vary based on the lender and the nature of the property.

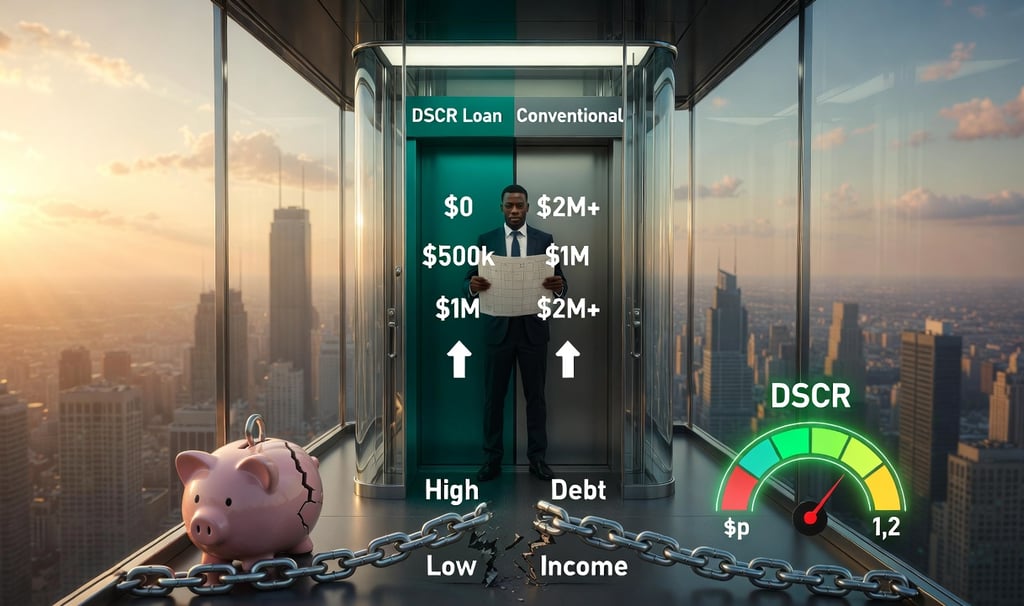

DSCR loans differ significantly from conventional financing methods, which often rely heavily on the borrower's credit score, employment history, and personal income. In contrast, DSCR-focused lenders prioritize the income generated by the property itself rather than the borrower's overall financial situation. This makes DSCR loans particularly attractive to real estate investors who may have a robust portfolio generating rental income but face challenges in showing sufficient personal income or creditworthiness.

The primary audience for DSCR loans includes real estate investors seeking a streamlined financing option that accommodates the realities of property income management. Investors intent on expanding their holdings, particularly those operating in markets where cash flow can fluctuate, find DSCR loans to be a critical tool in their investment strategy.

Benefits of DSCR Loans for Investors

Debt Service Coverage Ratio (DSCR) loans have emerged as a pivotal financing option for real estate investors. One significant advantage is their capacity to allow investors to secure properties without the stringent income verification typically required in traditional lending scenarios. This opens a pathway for individuals who may possess substantial investment potential but have atypical income streams, such as freelancers or entrepreneurs. By assessing the property's cash flow rather than personal income, these loans focus primarily on the property's ability to generate revenue, making them an appealing choice for many investors.

Another compelling benefit of DSCR loans is their ability to facilitate property acquisitions even when investors carry higher existing debts. Traditional lenders often impose limits or express hesitation toward those with elevated debt levels, fearing they may overextend financially. In contrast, since DSCR loans prioritize the income generated from the investment property, investors can leverage their existing assets to continue expanding their portfolios, thereby optimizing cash flow management. This flexibility is essential for individuals looking to build wealth through real estate.

Using DSCR loans can also assist investors in scaling their portfolio sizes more quickly. With competitive interest rates and beneficial repayment terms, these loans afford investors the opportunity to allocate resources towards acquiring additional properties rather than being burdened by extensive financing processes. For instance, an investor identifying a multi-family property that generates significant rental income may utilize a DSCR loan to secure the purchase, thus effectively increasing their presence in the real estate market. Overall, investing through such financing mechanisms not only enhances cash flow but also provides a sustainable model for progressive growth in the competitive realm of property investment.

Strategizing Investment Growth with DSCR Loans

DSCR loans, or Debt Service Coverage Ratio loans, can significantly enhance the financial landscape for real estate investors, enabling them to achieve investment growth even in challenging economic conditions. One pivotal strategy involves refinancing existing properties. By doing so, investors can unlock equity tied up in their current assets, thereby providing liquidity that can be utilized to finance new investments. This approach not only optimizes cash flow but also aids in enhancing the return on equity by allowing investors to leverage their existing portfolios.

Additionally, utilizing cash flows from rental income presents another strategic advantage. Investors can channel these earnings to facilitate the acquisition of additional properties, thereby creating a cycle of continuous growth. This is particularly advantageous when pursuing properties that generate a higher income than their acquisition costs, effectively improving the overall cash flow position.

Managing debt-to-income ratios is crucial when employing DSCR loans for investment purposes. Investors must ensure that their rental income sufficiently covers their debt obligations while maintaining a favorable ratio. A ratio above one indicates that the property generates enough income to cover its debts, a crucial factor for lenders. Thus, a disciplined approach to assessing potential investments is essential, weighing the risks against the projected rewards.

Furthermore, managing multiple investments requires meticulous planning and portfolio diversification. By strategically spreading investments across various property types and locations, investors can mitigate risks associated with market fluctuations and tenant turnover. This not only safeguards their investments but also positions them for sustained growth.

In essence, executing these strategies involves a comprehensive understanding of the dynamics of DSCR loans. By planning for long-term sustainability and staying informed, investors can effectively navigate their investment journeys and harness the full potential of their financial resources.

Real-Life Case Studies of Successful DSCR Loan Utilizations

In the realm of real estate investment, the ability to leverage debt wisely often determines success. Many investors have turned to Debt Service Coverage Ratio (DSCR) loans as a means to scale their portfolios even when faced with challenges like high existing debt or low income. Here, we explore several real-life case studies that showcase how these loans can facilitate growth in various market conditions.

One notable investor, Angela Smith, began her journey with a modest property portfolio largely funded through traditional loans. However, with a high debt-to-income ratio, she struggled to secure conventional financing for additional properties. Upon learning about DSCR loans, Angela pivoted her strategy. By focusing on the projected rental income from her properties rather than her personal income, she successfully secured financing for three additional rental units in a growing suburb. After renovating these units and optimizing their rental listings, her monthly income dramatically increased. Angela's case highlights the importance of understanding cash flow from investments rather than solely personal financial metrics.

Another compelling story is that of Tom Green, who faced a different set of challenges. As a first-time investor, Tom was hesitant due to his low income from a full-time job. However, he identified a multifamily property that generated significant rental revenue. With guidance on utilizing DSCR loans, Tom was able to purchase the property despite his income constraints. The successful acquisition allowed him to establish a steady cash flow, which not only increased his confidence but also improved his overall financial standing. Tom’s experience illustrates how strategic investment decisions, supported by DSCR financing, can empower individuals to transcend initial economic limitations.

These stories emphasize key lessons for aspiring investors: understanding the importance of cash flow dynamics, leveraging DSCR loans effectively, and making informed real estate choices regardless of initial financial setbacks. Experience from Angela and Tom serves as practical takeaways to navigate potential hurdles in the investment landscape.

Contact

Helping you secure smart commercial loans

Phone

info@belllending.com

682-312-4533

© 2026. All rights reserved.